As an independent contractor, you’re essentially running your own business—and that means you’re responsible for your protection. Unlike traditional employees, you don’t have built-in insurance coverage from an employer. One lawsuit, accident, or unexpected event could derail your finances and reputation. That’s where independent contractor insurance comes in. Depending on your industry, you may need general liability, professional liability, commercial auto, tools, and equipment, or even workers’ comp if you hire others.

Some of the best insurance providers for independent contractors in 2025 include Next Insurance, Hiscox, Thimble, Nationwide, and Progressive—known for affordable plans, fast quotes, and flexible coverage options. Protecting yourself is more than a legal checkbox—it’s about long-term success and peace of mind. Let’s answer the top questions contractors have about getting insured.

Understanding Independent Contractor Insurance

Independent contractors, freelancers, and self-employed individuals often work without the safety net of an employer-provided benefits package. Independent Contractor Insurance serves as a financial safeguard that covers the risks associated with working independently.

This insurance is essential because independent workers are legally liable for damages or claims arising from their services, property use, or mistakes. Whether you’re a graphic designer, consultant, handyman, or IT professional, having appropriate insurance ensures protection against lawsuits, accidents, and professional errors.

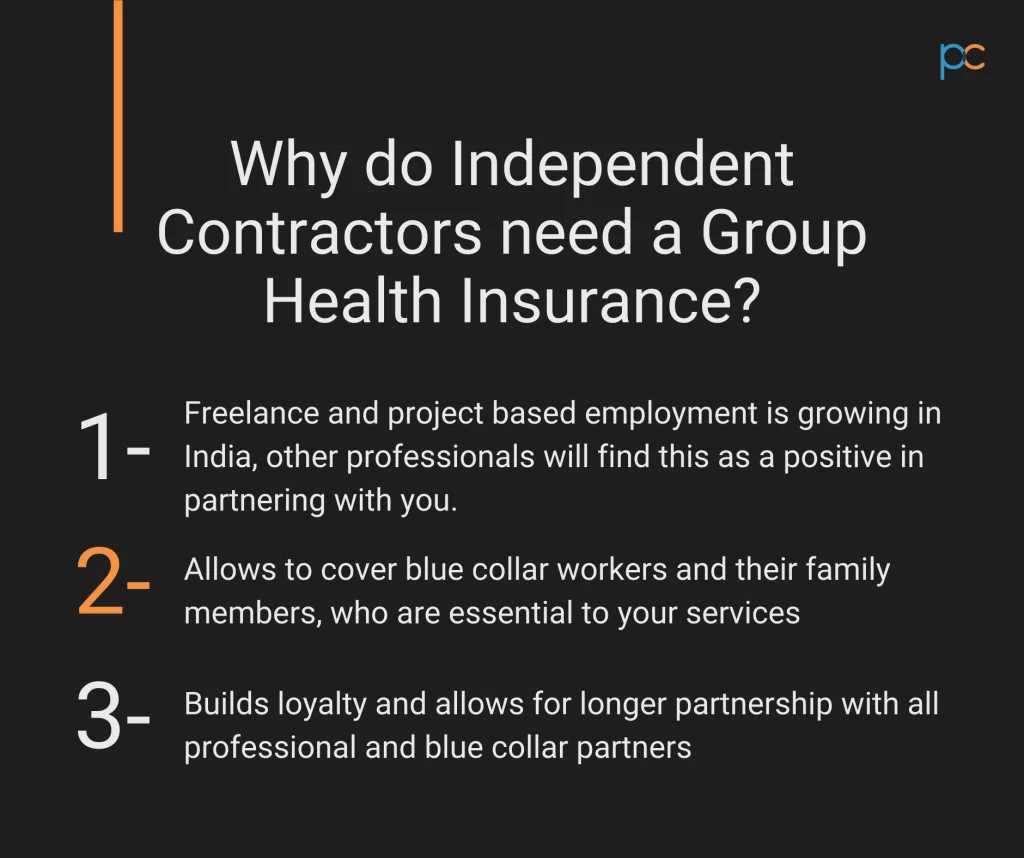

Why Independent Contractors Need Insurance

Independent contractors operate as self-employed professionals, which means they are personally liable for mistakes, property damage, or injuries related to their work. Unlike employees covered under an employer’s liability policy, contractors must carry their insurance.

Here’s why insurance is essential:

- Legal Protection: In case of lawsuits for negligence or property damage.

- Client Requirement: Many clients won’t hire uninsured contractors.

- Contract Obligations: Government or corporate contracts often demand proof of insurance.

- Business Continuity: Insurance helps cover damages or interruptions that could otherwise derail your work.

Types of Insurance Coverage You May Need

Independent contractors may need one or more types of insurance depending on the industry they operate in. Key coverages include:

- General Liability Insurance: This covers bodily injury, property damage, and legal fees if you’re held liable for an accident.

- Professional Liability Insurance (Errors & Omissions): Protects against claims of negligence, mistakes, or failure to deliver promised services.

- Commercial Auto Insurance: Required if you use your vehicle for work-related tasks.

- Workers’ Compensation: Mandatory in many states if you have employees; also beneficial for covering injuries to yourself on the job.

- Tools and Equipment Insurance: Covers damage or theft of your business tools.

- Cyber Liability Insurance: Vital for contractors who handle sensitive client data or operate online services.

How to Determine the Right Coverage for You

Choosing the right insurance coverage depends on several factors, including your profession, the level of risk involved in your work, whether you operate on client property, and whether you have subcontractors or employees. A construction contractor might need more comprehensive coverage compared to a freelance writer, for example. Begin by assessing:

- What liabilities do you face in daily operations

- Whether clients require specific insurance policies

- The value of tools or equipment used

- Your potential for professional errors or omissions

- The volume of sensitive data you handle

Benefits of Having Independent Contractor Insurance

Carrying proper insurance offers numerous advantages:

- Legal Protection: Shields you from the high cost of lawsuits and legal defense.

- Credibility and Trust: Clients prefer working with insured contractors, seeing them as professional and reliable.

- Business Continuity: Helps maintain your operations even after unexpected losses or incidents.

- Financial Security: Prevents out-of-pocket expenses from depleting your savings or business revenue.

- Contract Requirements: Many clients won’t engage with uninsured contractors. Insurance allows you to bid on more jobs.

Best Insurance Companies for Independent Contractors

While the “best” company varies depending on your needs, some top-rated insurers for independent contractors based on affordability, coverage options, and customer satisfaction include:

- Hiscox is known for its professional liability and general liability, which is tailored to freelancers and small businesses.

- Following Insurance – Offers an easy online application, transparent pricing, and instant certificate of insurance.

- Thimble – Great for on-demand coverage and flexible short-term policies.

- Hartford is a trusted name with a wide range of coverage, especially for construction and skilled trades.

- Progressive Commercial – Ideal for contractors who need commercial auto insurance with other coverages.

- State Farm – Good for those wanting local agent support and a range of bundled policies.

Cost of Independent Contractor Insurance

The cost of insurance for independent contractors depends on various factors such as your industry, location, coverage limits, and claims history. On average:

- General liability insurance might cost between $400 and $1,200 per year.

- Professional liability insurance ranges from $500 to $2,000 annually.

- Commercial auto insurance can vary widely but often starts around $1,000/year.

Insurance as a Strategic Investment

For independent contractors, insurance isn’t just a precaution—it’s a strategic asset. It ensures business continuity, legal compliance, and client confidence. Without employer support, independent professionals must proactively secure their livelihoods. By understanding your risks and selecting the right policies, you protect both your personal finances and professional reputation.

As more people enter the gig economy or pursue self-employment, insurance has become a necessary tool for success. Whether you’re just starting or expanding your independent contracting business, investing in the right insurance coverage is one of the most intelligent decisions you can make.

Frequently Asked Questions

Do I legally need insurance as an independent contractor?

It depends on your industry and state laws, but many clients require proof of insurance.

What types of insurance do contractors typically need?

General liability, professional liability, commercial auto, and sometimes workers’ comp or equipment coverage.

What does general liability cover?

It protects against third-party claims for bodily injury, property damage, and personal injury.

How is professional liability different?

It covers errors, omissions, or negligence in your professional services.

What if I use my car for work?

You may need commercial auto insurance, as personal policies often exclude work-related use.

Can I get insured quickly and affordably?

Yes—providers like Next, Thimble, and Hiscox offer fast, customizable coverage online.

Is insurance tax-deductible?

Yes—most business insurance premiums are deductible as business expenses.

What if I hire subcontractors occasionally?

You may need additional coverage or proof of insurance from them.

How much does contractor insurance cost?

It varies, but many basic plans start around $25–$50/month, depending on your risk level.

Can I cancel or adjust coverage anytime?

Many modern insurers offer monthly plans with flexible terms and no long-term contracts.

Conclusion

Independent contractor insurance isn’t just bright—it’s essential. From lawsuits to damaged tools or client disputes, the right coverage shields your finances and keeps your business running smoothly. With modern providers offering affordable, tailored plans, getting insured is easier than ever. Whether you’re a graphic designer or a general contractor, having protection in place boosts your credibility and helps you focus on what matters most—doing great work. Take the time to explore your options, get a few quotes, and build a policy that fits your business and budget.